Study by Alumnus Benjamin Keys (PhD '09) Cited in The New York Times

Alumnus Benjamin Keys (PhD ’09), now an assistant professor of real estate at the University of Pennsylvania’s Wharton School, released a study entitled, “Minimum Payments and Debt Paydown in Consumer Credit Cards.” His study examining the credit card payment behavior of consumers was cited in The New York Times’ article “The Persistence of the Minimum Payment”.

According to Keys’ study, roughly a third of consumers pay an amount close to the minimum monthly payment regardless of whether they can afford to pay more. This results in more interest and paying more for an item in the long run. He found that 9 to 20 percent of consumers can afford to pay more but do not due to a fixation on the minimum payment, “They use the minimum payment as a guide, or anchor,” said Keys.

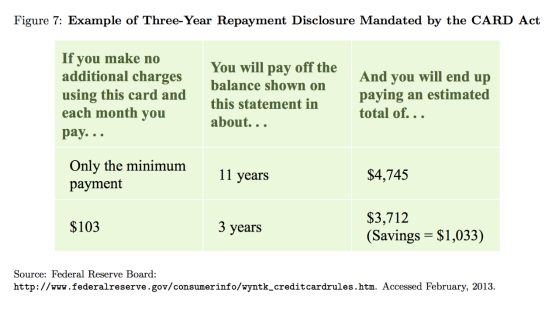

Even with the edition of the 2009 Credit CARD Act, where consumers see the amount of interest saved and monthly payment required to pay off debt in three years, less than 1 percent altered their payment behavior.

Keys found that 10 percent of consumers, from the sample of one-quarter of the US general-purpose credit card market, were anchored to the minimum payment. He found that consumers still met the minimum payment, regardless of whether it was increased or decreased. Read “Minimum Payments and Debt Paydown in Consumer Credit Cards” for all of Keys’ findings.

Abstract

Using a dataset covering one quarter of the U.S. general-purpose credit card market, we document that 29% of accounts regularly make payments at or near the minimum payment. We exploit changes in issuers' minimum payment formulas to distinguish between liquidity constraints and anchoring as explanations for the prevalence of near-minimum payments. Nine to twenty percent of all accounts respond more to the formula changes than expected based on liquidity constraints alone, representing a lower bound on the role of anchoring. Disclosures implemented by the CARD Act, an example of one potential policy solution to anchoring, resulted in fewer than 1% of accounts adopting an alternative suggested payment. Based on back-of-envelope calculations, the disclosures led to $62 million in interest savings per year, but would have saved over $2 billion per year if all anchoring consumers had adopted the new suggested payment. Our results show that anchoring to a salient contractual term has a significant impact on household debt.

Read “The Persistence of the Minimum Payment” from The New York Times